Saudi Arabia’s defence industry is changing fast under Vision 2030. The goal is clear: localize 50 percent of military procurement by 2030 under the aegis of GAMI and SAMI. Saudi Arabia is also ranked as the fifth-largest defense spender in the world in 2023, and its 2025 budget allocated $72.5 billion to defense spending, about 21.2 percent of the total budget. These conditions make the country a major target for deals, partnerships, and Saudi defence sector M&A.

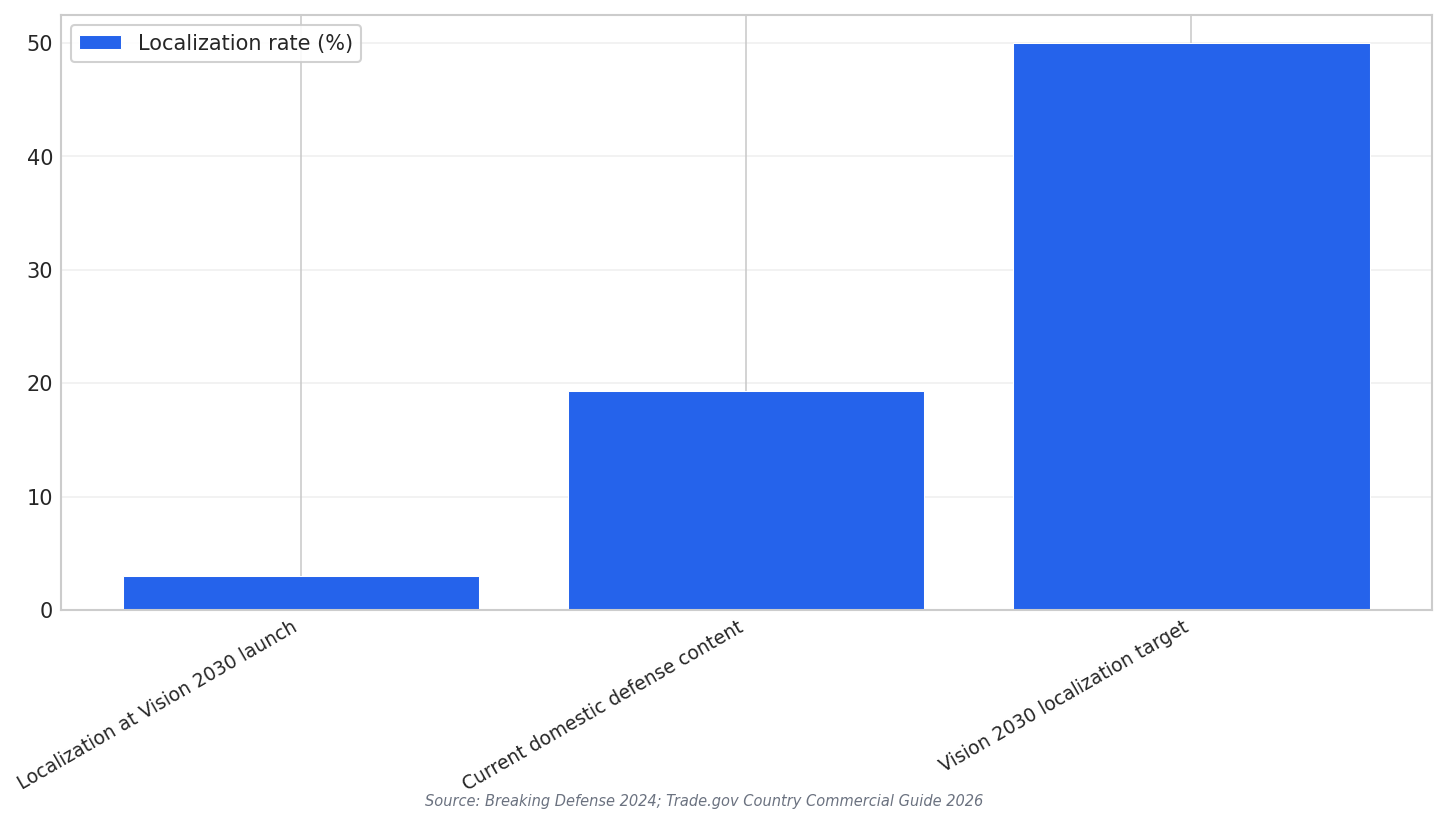

One simple way to see the shift is through localization levels. When Vision 2030 was launched, localization was about 3 percent. Domestic defense content has now reached 19.35 percent. The national target remains 50 percent by 2030. These are three distinct milestones that help explain why capability-building moves, including acquisitions, matter.

SAMI was launched in May 2017 by the Public Investment Fund as a state-owned defence company to reduce reliance on foreign purchases. It operates across aeronautics, land systems, weapons and missiles, and defense electronics. Vision 2030.ai also describes SAMI’s approach as a mix of joint ventures, technology transfer agreements, acquisitions, and organic capability development. This mix is important because Saudi procurement is often negotiated on a case-by-case basis in practice, even though legislation exists.

In Saudi defence sector M&A, the most visible example is SAMI’s acquisition of Advanced Electronics Company (AEC). SAMI said the deal supports its plan to expand and enter the Defense Electronics sector. The announcement described it as the largest military industries deal ever concluded in the Kingdom of Saudi Arabia. It was expected to complete in the first quarter of 2021 following regulatory approvals, and it would make AEC a 100% Saudi-owned company. SAMI also highlighted AEC’s 32-year experience in the military industries market.

Why Partnerships and Deals Matter Under Vision 2030

SAMI’s deal-making sits beside a wide partnership strategy. In May 2017, it signed MOUs with Boeing, Lockheed Martin, Raytheon, and General Dynamics. In October 2017, it signed an MOU with Russia’s Rosoboronexport covering technology transfer for local production of systems including the S-400 Triumf and the AK-103. In January 2018, SAMI agreed to joint ventures with Thales and John Cockerill, with stated localization ratios of 70% and 60%. In November 2018, SAMI and Navantia announced a joint venture linked to designing and building 5 Avante 2200 corvettes for the Ministry of Defense.

SAMI also ties these moves to scale. CEO Walid Abukhaled said SAMI started operations in January 2018, and that revenue has been growing 21 percent year over year. He also cited a backlog of about 15 billion riyal ($4 billion) and contracts won last year of about 9 billion riyal. He said SAMI became number 98 globally after four years of starting operation, then climbed to number 79. Across sources, SAMI’s ambition is consistent: to become one of the top 25 defense companies in the world by 2030.

What does Saudi defence sector M&A mean in the Vision 2030 context?

What is Saudi Arabia’s localization goal for military procurement by 2030?

What is the current domestic defense content level mentioned in the sources?

What did SAMI say its acquisition of AEC would achieve?

Which figures did SAMI’s CEO share about backlog and contract wins?

Talk to us for your needs in:

-

Due Diligence and Valuation Services

-

M&A Strategy and Advisory

-

Post-Merger Integration Management

-

Regulatory and Compliance Advisory

-

Market Entry and Expansion Consulting

-

Investment and Financial Analysis

-

In-Depth Market Survey for M&A

-

Market Intelligence and Insights in M&A

-

Feasibility Study and Assessment in M&A

-

Saudi M&A Benchmarking