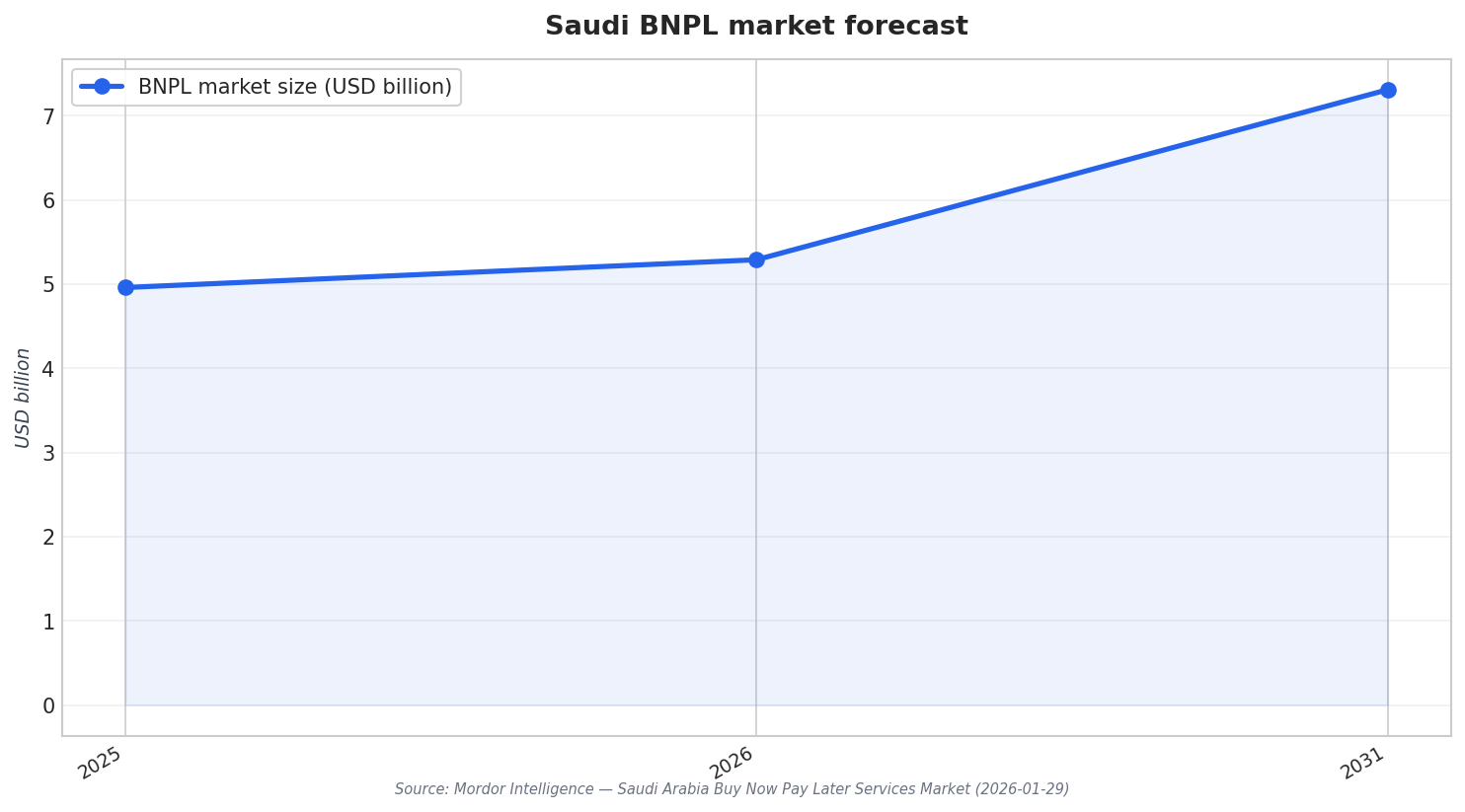

Saudi Arabia’s buy-now-pay-later (BNPL) sector is expanding, but the conditions around it increasingly resemble a market that will reward scale. Mordor Intelligence estimates the Saudi Arabia BNPL market at USD 4.96 billion in 2025 and USD 5.29 billion in 2026, with a projection of USD 7.31 billion by 2031 at a 6.66% CAGR for 2026–2031. A separate ResearchAndMarkets.com press release expects the BNPL payment market to reach US$10.71 billion in 2026 and projects growth from USD 9.56 billion in 2025 to about USD 16.69 billion by 2031 at a 9.3% CAGR. Across these differing estimates, the direction is consistent: more volume, more providers, and stronger pressure for the leaders to separate from the pack.

Demand-side signals also point to a market where BNPL can become a default checkout feature, not a niche option. Mordor reports Saudi online retail sales jumped 78.3% to SAR 37.02 billion (USD 9.87 billion) in 2024, and notes that Checkout.com attributes a 20–30% lift in merchant conversion rates when BNPL is embedded at checkout. Vision 2030’s cashless push is cited as another tailwind: the same source says the 70% non-cash transactions goal was surpassed in 2024, with electronic payments accounting for 79% of all transactions. With smartphone penetration topping 98% in the report, app-based onboarding and instant decisions reinforce the advantage of brands that can win consumer mindshare and merchant placement.

Why Scale and Regulation Favor Fewer Winners

Regulation and market structure can accelerate consolidation by raising the bar for compliance, underwriting discipline, and distribution. Mordor references SAMA’s 2023 licensing framework and says it governs 67 finance companies, positioning consumer protection and disciplined underwriting as part of the market’s “mature phase.” At the same time, the channel split highlights why merchant integration matters: online platforms accounted for 60.74% of market share in 2025, while point-of-sale installations are projected to advance at a 24.12% CAGR through 2031. End-use concentration is also visible, with fashion and personal care at 37.18% of market size in 2025, while healthcare financing is forecast to expand at a 33.97% CAGR to 2031—an attractive growth lane that may reward providers capable of building specialized partnerships.

This backdrop explains why Tamara and Tabby keep showing up as anchors of the Saudi competitive story. The AI Journal describes the market as being driven by established players such as Tamara and Tabby, alongside new entrants like Postpay and Spotti, and it flags strategic acquisitions and product launches as signals of an evolving landscape. Specifically, it cites Tamara’s acquisition of PayTabs and ToYou’s entry into BNPL. Nexdigm similarly describes the market as concentrated around a few major players—Tamara, Tabby, Spotti, Postpay, and STC Pay—and ties their dominance to consolidation and maturity, alongside high entry barriers in consumer adoption and merchant partnerships. It also notes Saudi Arabia had 157.8 mobile cellular subscriptions per 100 people in 2023, up from 149.8 in 2022, underscoring the reach of mobile-first distribution.

Over the next phase, the most durable advantage may come from breadth: channel coverage, category depth, and funding or partnerships that support larger merchant networks. Mordor reports pure-play fintechs held 46.97% share in 2025, but bank-affiliated BNPL services have the highest projected CAGR at 28.85% through 2031, pointing to rising competition from traditional finance. Regionally, central province led with 31.02% revenue share in 2025, while northern province is poised for a 28.81% CAGR, linked in the report to NEOM and Red Sea megaprojects. In that environment, Saudi BNPL consolidation becomes a practical outcome of scaling economics: providers that combine regulation-ready operations with distribution and category partnerships are better positioned to absorb rivals or outcompete smaller platforms.

What do the sources say about Saudi Arabia’s BNPL market size and growth?

What is driving BNPL adoption in Saudi Arabia according to the sources?

Which companies are described as leading players in Saudi BNPL?

What signals suggest consolidation is coming in Saudi Arabia’s BNPL sector?

How are scale and regulation shaping Saudi BNPL consolidation?

Talk to us for your needs in:

-

Due Diligence and Valuation Services

-

M&A Strategy and Advisory

-

Post-Merger Integration Management

-

Regulatory and Compliance Advisory

-

Market Entry and Expansion Consulting

-

Investment and Financial Analysis

-

In-Depth Market Survey for M&A

-

Market Intelligence and Insights in M&A

-

Feasibility Study and Assessment in M&A

-

Saudi M&A Benchmarking