Saudi Arabia’s market reforms under Vision 2030 aim to attract more foreign investment and improve transparency, investor protection, and corporate governance. Walid Majdalani, head of emerging markets PE at Investcorp, described these changes as positive steps in becoming a mature market and tied them to increased liquidity and market credibility. For private equity, deeper liquidity matters because it can make larger IPOs easier to execute and public exits more viable. Suveer Arenja of FIM Partners said exits have long been a question mark, with investors often relying on opportunistic trade sales, but that the IPO market is increasingly viewed as a credible exit route.

That maturing backdrop sits alongside a tougher global exit environment that is pushing sponsors toward alternative liquidity tools. Privateequitywire reported that buyout groups completed disposals worth roughly $103bn in the first quarter, a decline of around 36% compared with the same period last year. The same report said activity between financial sponsors has been noticeably subdued, making it harder to distribute capital and restart fundraising cycles. In response, firms are adopting minority stake sales and continuation vehicles to partially realise value without a full sale. This matters for Saudi secondary buyouts because sponsor-to-sponsor routes and structured secondaries can bridge timing gaps when traditional exits slow.

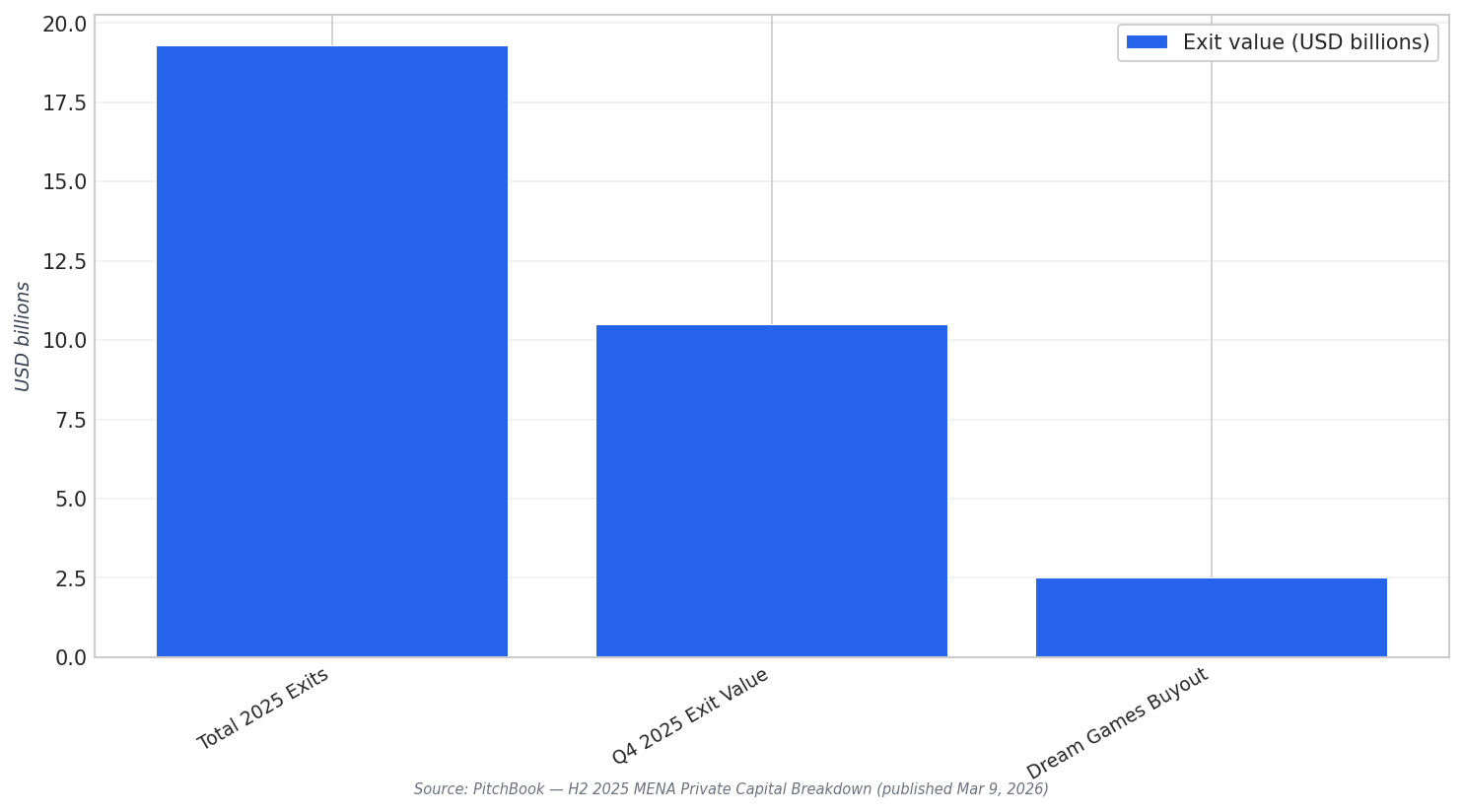

In MENA, PitchBook’s H2 2025 breakdown showed exit activity rebounded, generating $19.3 billion across 93 PE and VC exits. A bumper Q4 delivered $10.5 billion in exit value, supported by PE-backed listings and CVC’s $2.5 billion buyout of Dream Games. The same report noted fundraising pressure, with capital raised falling 60.2% YoY to $6.6 billion and median fund close times stretching to 34 months. This combination creates a clear incentive to engineer liquidity in more than one way, including Saudi secondary buyouts and continuation-style solutions that can return cash to LPs while keeping assets on a value-creation path.

Continuation Vehicles and Secondaries: Liquidity Without Letting Go

Continuation vehicles have become a prominent tool for sponsors that want liquidity but do not want to exit entirely. Bain reported that secondaries expanded as an exit channel in 2025, with transaction value of GP- and LP-led vehicles growing 41% year over year. Bain also said GP-led continuation vehicles grew 62% year over year and 37% annually since 2022, while still accounting for less than 10% of total PE exit value today. This supports the idea that Saudi secondary buyouts will increasingly sit alongside IPO exits, not replace them, especially as the market becomes more liquid and deal structures become more complex.

Secondaries bring their own mechanics and risks. The Financial Times noted that secondaries funds often invest in later-stage holdings closer to exit, aiming to pay back cash faster, sometimes by buying at slight discounts and using leverage. It also highlighted that continuation vehicles can deploy significant leverage and that such deals can be financed with about 50% debt. A private equity executive warned about over-reliance on leverage if the wrong assets are selected, since downside can be amplified if companies underperform or cannot be sold at expected valuations. For Saudi secondary buyouts, this reinforces the need for disciplined pricing, governance, and underwriting.

Saudi Arabia’s pipeline for listings also signals a broader exit toolkit forming across public and private markets. Arab News reported that Saudi Arabia achieved a record number of deals in 2024 at 178, representing 31% of MENA’s total deal number. The same source said more than 50 IPO applications were under review by the regulator and the exchange. Together with reforms aimed at transparency and investor protection, these indicators support a more credible environment for exits. In practice, sponsors can pair IPO readiness with Saudi secondary buyouts and continuation vehicles to manage timing, return capital, and maintain exposure to long-term upside.

What are Saudi secondary buyouts in today’s exit environment?

Why are continuation vehicles becoming more common?

How strong was MENA exit activity in 2025?

What is a key risk to watch in continuation vehicles?

What signals point to a stronger Saudi IPO pipeline?

Talk to us for your needs in:

-

Due Diligence and Valuation Services

-

M&A Strategy and Advisory

-

Post-Merger Integration Management

-

Regulatory and Compliance Advisory

-

Market Entry and Expansion Consulting

-

Investment and Financial Analysis

-

In-Depth Market Survey for M&A

-

Market Intelligence and Insights in M&A

-

Feasibility Study and Assessment in M&A

-

Saudi M&A Benchmarking