Saudi hospitality M&A is moving from single-asset deals toward platform and portfolio logic. Vision 2030 is accelerating development, and investors are aligning acquisition and partnership strategies with long-duration demand drivers. Industry commentary links this momentum to Expo 2030 and ongoing Vision 2030 initiatives, with operators stating they are investing heavily to grow their brand footprint. At the same time, the country is not simply adding inventory; it is reshaping how tourism, culture, infrastructure, entertainment, and capital combine to create long-term value. In this context, hotel portfolio plays can be a faster route to market presence than building asset by asset.

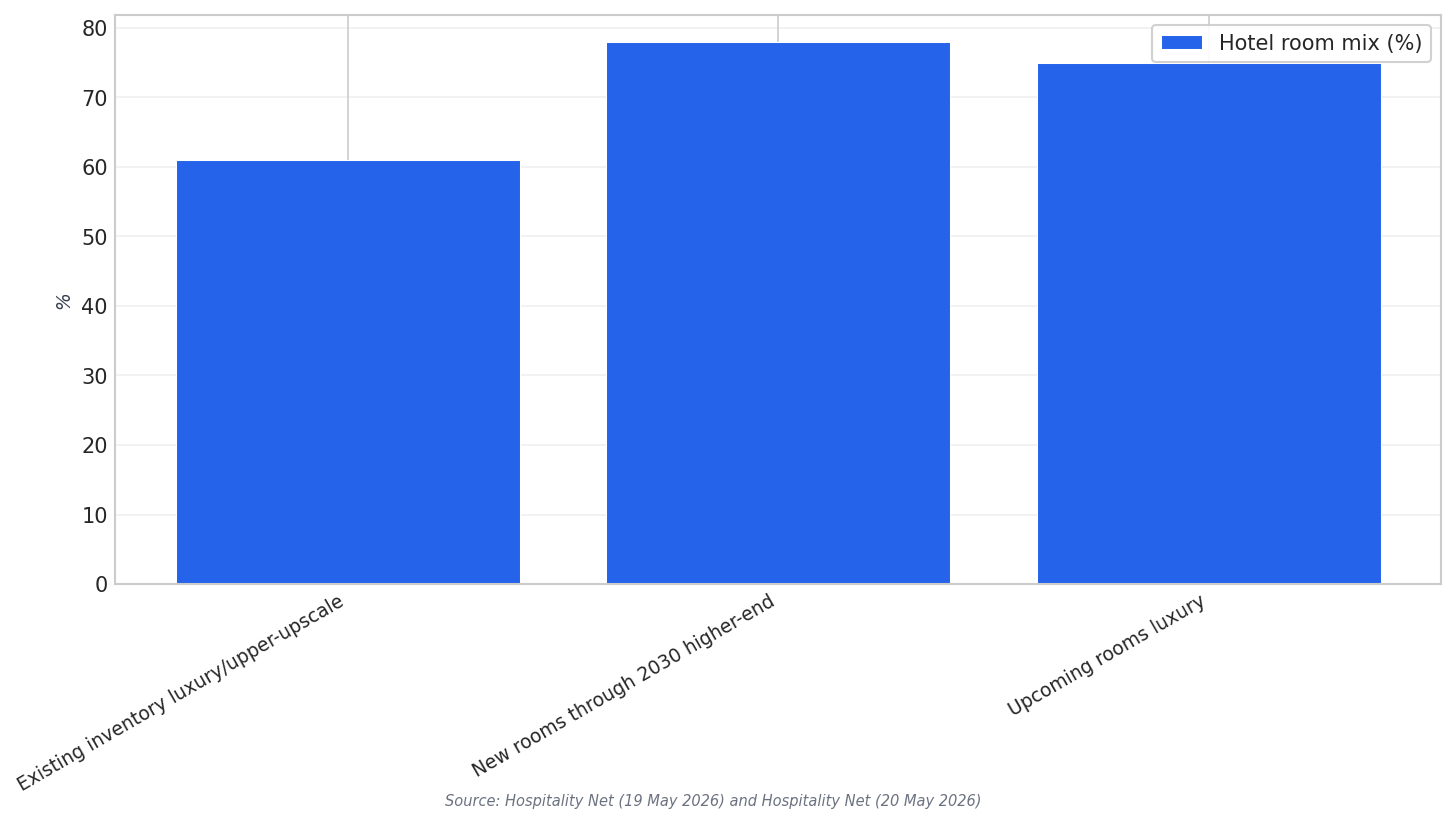

Supply composition is a key driver behind portfolio positioning. Sources indicate that around 61% of existing hotel inventory is concentrated in luxury and upper-upscale segments. They also note nearly 78% of new rooms through 2030 are planned at the higher end. Another viewpoint highlights that 75% of upcoming hotel rooms are in the luxury segment. This imbalance is why multiple experts point to midscale as a scalable opportunity. One CEO frames the “biggest opportunity” as scalable midscale in cities with real demand drivers, arguing that efficiently operated hotels can deliver stable occupancy and repeat business without relying on luxury-rate assumptions.

These points can be read as an M&A signal: portfolios weighted to mid-market, conversions, and adaptive reuse can help rebalance exposure. Sector commentary describes “asset transformation” as a defining feature of Tourism 2030 delivery, with conversions and adaptive reuse becoming increasingly central as owners exercise greater capital discipline. Deal teams can therefore look for under-managed assets that can be repositioned into scalable brands. Brand pipelines also reinforce the portfolio mindset. Hilton reports surpassing 100 hotels trading and in the pipeline in Saudi Arabia, with 21 operating and 83 in the pipeline, representing a combined investment of USD $8 billion from owners and investors.

Hotel Portfolio Plays: Cluster, Convert, and Partner

Portfolio plays in Saudi Arabia can also be built around destination clustering. HMH, founded in 2003 in Dubai, operates five brands and positions itself as the largest operator in the dry sector within the region. In Saudi Arabia, it highlights Corp Hotel Al Khobar in the Eastern Province, serving executives in oil, gas, and petrochemicals, and Corp Makkah Hotel minutes from Al-Masjid Al-Haram, serving pilgrims, tourists, and business visitors. This multi-demand mix supports the logic of city pairs and corridor portfolios. Corporate travel growth tied to new financial districts in Riyadh and mega-projects, plus Makkah’s millions of international visitors annually, strengthens the case for diversified portfolio exposure.

Public-sector backed development pipelines can also shape deal flow. Al Balad Development Company introduced a USD 3.6 billion hospitality investment portfolio in Jeddah’s historic Al Balad district. It plans to deliver more than 3,300 hotel units from mid-scale to luxury over 2025 to 2038 using models including public-private partnerships, investment funds, and joint ventures. Separately, Future Hospitality Summit commentary points to a USD $10 billion tourism development pipeline and the target to deliver over 362,000 new hotel rooms by 2030. In 2025, Saudi Arabia welcomed 122 to 123 million domestic and international tourists and generated SAR 300 billion in tourism spending, reinforcing why investors are preparing now for Expo 2030-era demand volatility and opportunity.

What is driving Saudi hospitality M&A ahead of Expo 2030?

Why is midscale frequently mentioned as an opportunity in Saudi Arabia?

What does the supply mix look like in the available sources?

Which deal structures are highlighted for hospitality investment in Jeddah’s Al Balad district?

How large is Hilton’s stated Saudi Arabia footprint in the sources?

Talk to us for your needs in:

-

Due Diligence and Valuation Services

-

M&A Strategy and Advisory

-

Post-Merger Integration Management

-

Regulatory and Compliance Advisory

-

Market Entry and Expansion Consulting

-

Investment and Financial Analysis

-

In-Depth Market Survey for M&A

-

Market Intelligence and Insights in M&A

-

Feasibility Study and Assessment in M&A

-

Saudi M&A Benchmarking