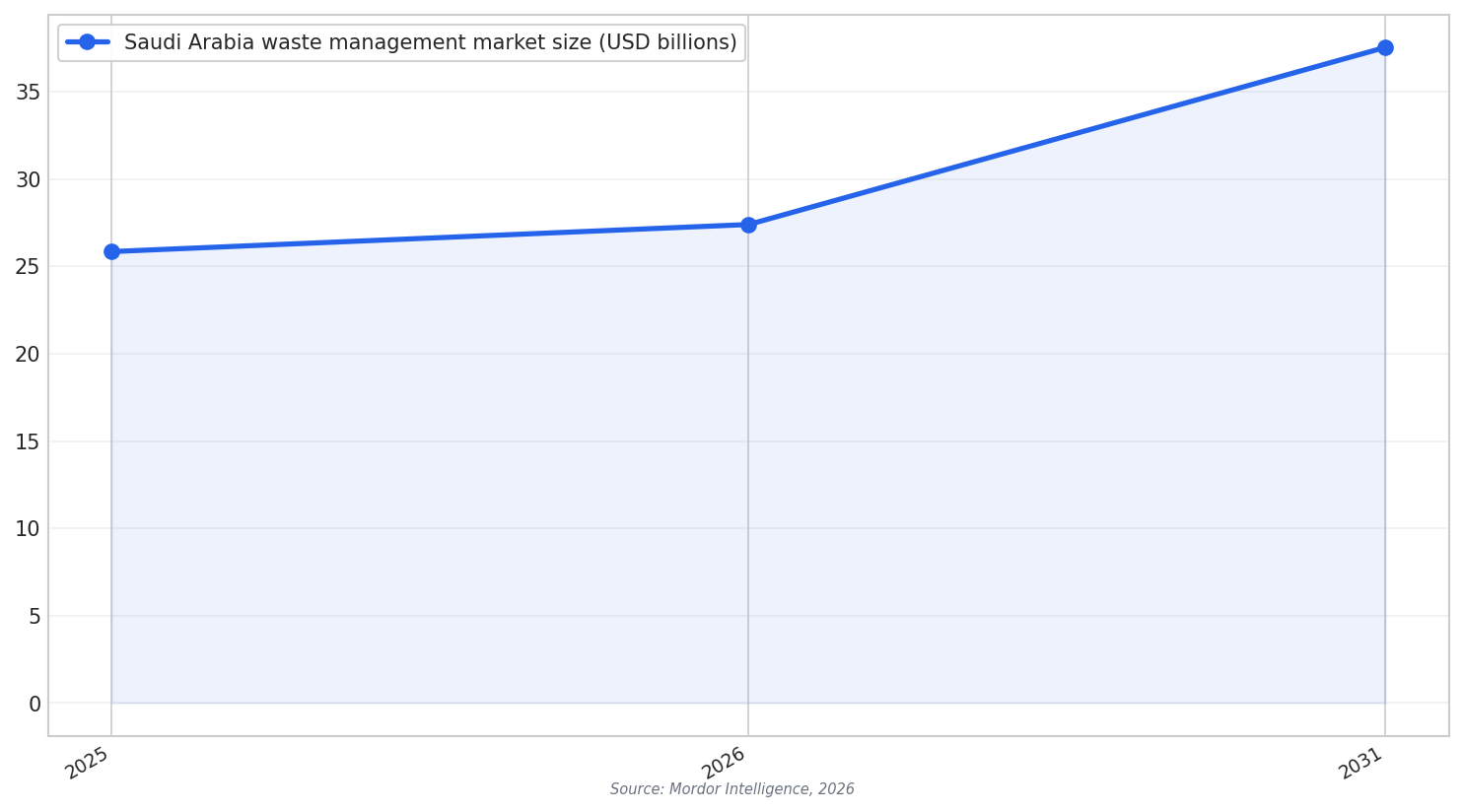

Saudi Arabia’s waste sector is shifting from basic collection and landfilling toward more organized systems. Mordor Intelligence values the Saudi Arabia waste management market at USD 25.84 billion in 2025, and estimates it will reach USD 37.53 billion by 2031. This change is tied to Vision 2030 pressure, stricter penalties under Royal Decree M/3, and a growing pipeline of public-private-partnership (PPP) projects. As the market grows, scale matters more. That is a key reason why consolidation and Saudi waste management M&A are becoming central topics.

The activity is also shaped by where waste volumes come from. In Mordor’s breakdown for 2025, residential waste held 55.35% of market share. Municipal solid waste (MSW) held 45.85%. Disposal and treatment services accounted for 53.45% of the market. Riyadh alone accounted for 38.5% of the market size. These shares show why operators want larger footprints and broader service lines, especially in major cities.

Market concentration is already visible. Mordor reports that Saudi Investment Recycling Company (SIRC), Veolia, SUEZ, Averda, and BEEAH collectively managed more than 50% of treated volumes in 2025. It also states that SIRC alone recycled 16 million tons of construction-and-demolition (C&D) waste in 2025. When a few groups manage a large share of treated volumes, buyers often seek more assets, routes, and facilities to defend their position and win new contracts.

Why Consolidation Pressure Is Rising

Regulation raises the cost of getting it wrong. Mordor notes that Royal Decree M/3 introduced fines up to USD 8 million and prison terms for non-compliance. At the same time, Arab News reports that the National Center for Waste Management (MWAN) oversees all waste types in the Kingdom excluding radioactive and military waste, across seven categories, including municipal solid waste, industrial waste, healthcare waste, sludge, agricultural waste, construction and demolition debris, and special waste such as tires and electronic devices. This wide scope increases the need for specialized capabilities, which can be easier to build through acquisitions and partnerships.

Demand pressure is also rising. EcoMENA states Saudi Arabia generates more than 15 million tons of solid waste per year, with per capita waste generation estimated at 1.5 to 1.8 kg per person per day. It adds that solid waste generation in Riyadh, Jeddah, and Dammam exceeds 6 million tons per annum. Mordor also expects per-capita MSW generation to rise from 1.4 kilograms per day in 2024 to 1.6 kilograms by 2030, alongside population growth above 36 million by 2030 and urban migration toward Riyadh, Jeddah, and Dammam.

Finally, the asset build-out is large, and that can favor bigger platforms. Arab News cites MWAN saying investment opportunities are estimated at about SR420 billion by 2040, and that Saudi Arabia currently has more than 230 landfills. Mordor links the shift away from uncontrolled landfilling to integrated resource recovery, and points to demand for mobile crushers, material recovery facilities (MRFs), and refuse-derived-fuel (RDF) plants as C&D waste grows from large construction programs such as NEOM and the Red Sea Project. In this environment, Saudi waste management M&A becomes a practical route to gain facilities, technology, and geographic coverage faster.

What is driving Saudi waste management M&A right now?

How big is Saudi Arabia’s waste management market?

Which segments hold the largest shares in 2025?

How concentrated is the industry among major operators?

What scale of investment opportunities is expected in the sector?

Talk to us for your needs in:

-

Due Diligence and Valuation Services

-

M&A Strategy and Advisory

-

Post-Merger Integration Management

-

Regulatory and Compliance Advisory

-

Market Entry and Expansion Consulting

-

Investment and Financial Analysis

-

In-Depth Market Survey for M&A

-

Market Intelligence and Insights in M&A

-

Feasibility Study and Assessment in M&A

-

Saudi M&A Benchmarking