In Saudi M&A, the headline price is not the full story. Zakat, VAT, and withholding tax (WHT) can change cash flow, affect valuation, and create closing friction. The core issue is that Saudi Arabia uses a dual-track system administered by the Zakat, Tax and Customs Authority (ZATCA). Saudi and GCC ownership is generally subject to Zakat, while non-Saudi and non-GCC ownership is subject to corporate income tax (CIT). This split matters in every acquisition model.

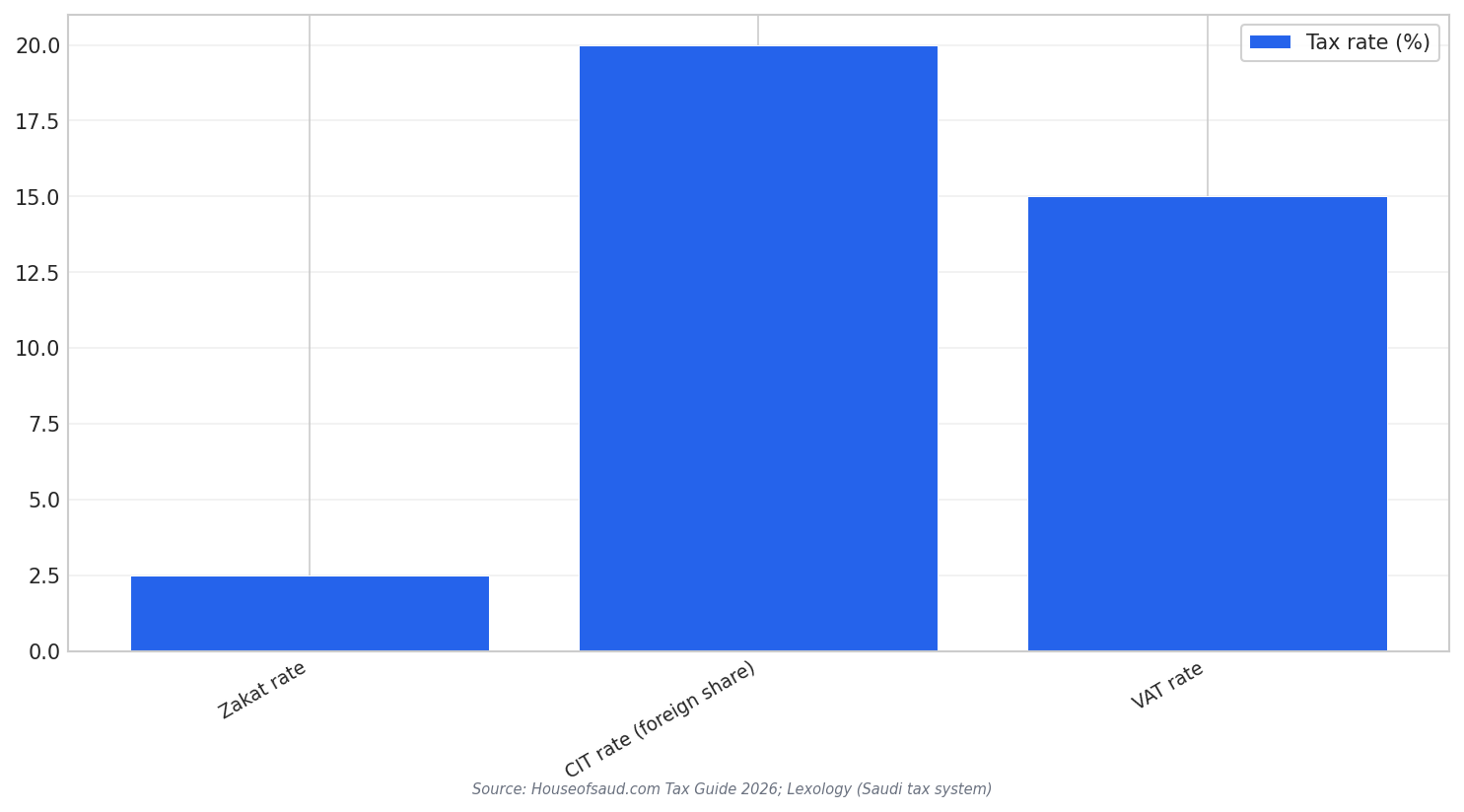

Rates are a practical starting point for due diligence. Zakat applies at 2.5% of the Zakat base for Saudi and GCC-owned shares. CIT applies at 20% on the taxable income share attributable to non-Saudi and non-GCC shareholders. VAT applies at 15% to most goods and services. WHT can apply to cross-border payments such as dividends at 5%, royalties at 15%, and management fees at 20% when paid to non-residents.

A common trap is assuming the target pays one “corporate tax.” In reality, mixed-ownership entities split obligations: the Saudi/GCC portion is subject to Zakat, while the foreign portion is subject to CIT. So a post-deal cap table change can change the tax mix even if the business operations do not change. Branches of foreign companies can also be a risk point, because they are treated as permanent establishments and are subject to 20% corporate tax, and they are exempt from Zakat since they are not owned by GCC nationals.

Withholding Tax: The Silent Purchase Price Adjuster

WHT is often where “leakage” happens in a cross-border deal. If the acquisition structure creates new non-resident payees, then dividends (5%), royalties (15%), and management fees (20%) may face WHT. This matters in post-close integration, where shared services and IP arrangements often drive large intercompany charges. Some structures try to treat certain fees as cost compensation, which may be exempt from WHT if they represent only costs, but the facts and documentation need to support that position.

Treaty access can also be a trap if it is assumed but not verified. One source notes that, as of 2025, Saudi Arabia has more than 50 double taxation treaties that foreign investors may use to lower WHT on items such as royalties, management fees, technical fees, or dividends, potentially reducing rates from 5–15% to as low as 0%. Another source states Saudi Arabia has signed over 60 double taxation treaties. Either way, “Saudi M&A tax structuring” should confirm treaty eligibility early and align the payment flows with the intended treaty outcome.

VAT is also relevant in transactions and integration. VAT at 15% applies to most goods and services, and businesses must register and report VAT transactions. Penalties can apply for late filings, non-payment, or inaccurate reporting. In a deal, the buyer typically wants comfort that the target’s VAT reporting and records are clean, because issues may surface after closing during audits and system migrations. ZATCA’s enforcement focus is not theoretical: one source reports ZATCA collected over SAR 600 billion in combined zakat, tax, and customs revenue in 2025.

What is the biggest risk in Saudi M&A tax structuring?

What is the VAT rate that can affect services and integration after a deal?

Which cross-border payments can trigger withholding tax in Saudi Arabia?

Can tax treaties reduce withholding tax in Saudi M&A?

Why should buyers care about ZATCA enforcement pressure?

Talk to us for your needs in:

-

Due Diligence and Valuation Services

-

M&A Strategy and Advisory

-

Post-Merger Integration Management

-

Regulatory and Compliance Advisory

-

Market Entry and Expansion Consulting

-

Investment and Financial Analysis

-

In-Depth Market Survey for M&A

-

Market Intelligence and Insights in M&A

-

Feasibility Study and Assessment in M&A

-

Saudi M&A Benchmarking