Special Economic Zones M&A Saudi deals can look simple at first. But the zone rules can change how a buyer prices the target, how the entity must be structured, and how money moves after closing. Saudi Arabia has activated implementing regulations for its Special Economic Zones (SEZs), published in the Official Gazette on January 16, 2026, with full effect in April 2026. These rules sit inside a broader Vision 2030 diversification drive.

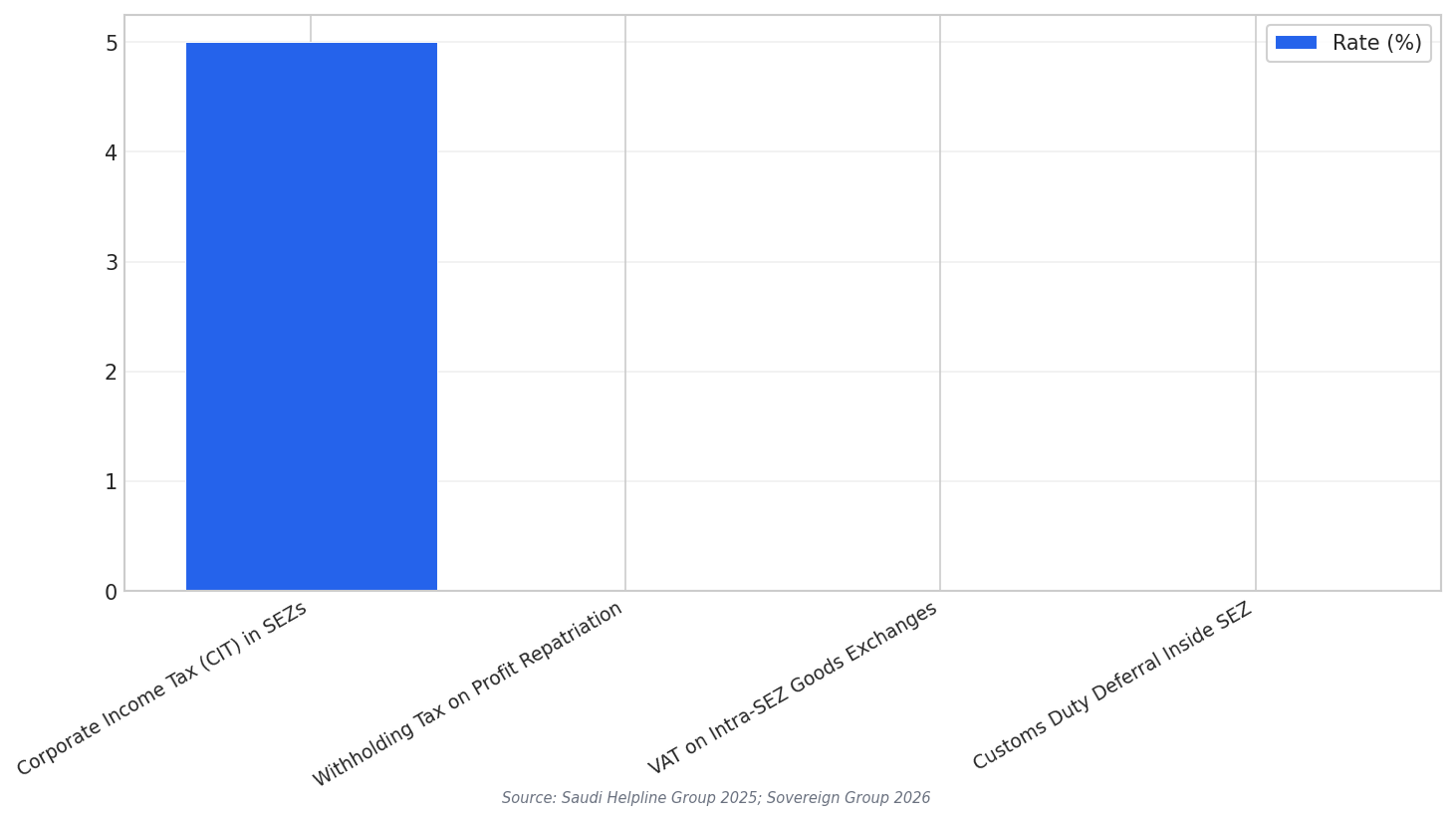

Across multiple sources, the headline incentives repeat in a consistent way. Companies in SEZs are described as benefiting from a 5% corporate income tax rate for up to 20 years, 0% withholding tax on profit repatriation, and 0% customs duties on capital equipment and inputs. Some sources also describe VAT relief on intra-zone activity and that goods traded and stored within SEZs are customs-free.

In plain numbers used in the sources, the core deal model is built around four rates: 5% corporate income tax, 0% withholding tax on profit repatriation, 0% VAT on intra-SEZ goods exchanged within and between zones, and 0% customs duty deferral for goods inside the SEZ. These figures often become the center of the investment case in an acquisition, because they shape forecast cash flow and post-deal distribution planning.

Ownership, Licensing, and What a Buyer Must Actually Acquire

Ownership and licensing are not side issues in an SEZ acquisition. Several sources state that Saudi SEZs allow 100% foreign ownership. Aurifer Tax adds a key operational point: to operate within an SEZ, entities must be incorporated as a Saudi limited liability company (LLC) with their principal place of business located within the zone. Aurifer Tax also says these zones are governed by the Economic Cities and Special Zones Authority (ECZA), which holds sole authority to issue licenses and permits.

For scope, Aurifer Tax lists four SEZs: King Abdullah Economic City (KAEC) SEZ, Jazan Special Economic Zone, Ras Al-Khair Special Economic Zone, and a Cloud Computing Special Economic Zone described as a “virtual” zone based in Riyadh. In M&A terms, this matters because the target’s licensed activity and location help define whether the buyer can keep the same incentives after closing.

Deal mechanics often turn on how the buyer expects to return cash to the parent. Middle East Briefing explains that wholly-owned foreign subsidiaries have control over dividend distribution decisions if they meet statutory reserve requirements and board approvals under the Saudi Companies Law. It also states that branches of foreign companies can transfer profits directly without formal dividend declarations, but they must show the funds are legitimate post-tax earnings. In the same source, Saudi Arabia’s dual tax system is described as corporate income tax at 20% on net adjusted profits for foreign companies and Zakat at 2.5% on the assessed base for local entities.

What are the key tax incentives used in Special Economic Zones M&A Saudi deals?

Can a foreign buyer own 100% of an SEZ company in Saudi Arabia?

Who issues SEZ licenses and permits in Saudi Arabia?

What entity form is required to operate inside a Saudi SEZ?

How can profits be repatriated after an acquisition?

Talk to us for your needs in:

-

Due Diligence and Valuation Services

-

M&A Strategy and Advisory

-

Post-Merger Integration Management

-

Regulatory and Compliance Advisory

-

Market Entry and Expansion Consulting

-

Investment and Financial Analysis

-

In-Depth Market Survey for M&A

-

Market Intelligence and Insights in M&A

-

Feasibility Study and Assessment in M&A

-

Saudi M&A Benchmarking