PropTech acquisitions KSA are no longer niche deals. They are becoming a core strategy for Saudi construction and logistics giants. Saudi Arabia’s PropTech market was valued at about USD 0.86 billion in 2024 and is expected to reach USD 2.48 billion by 2030, growing close to 19 percent annually.

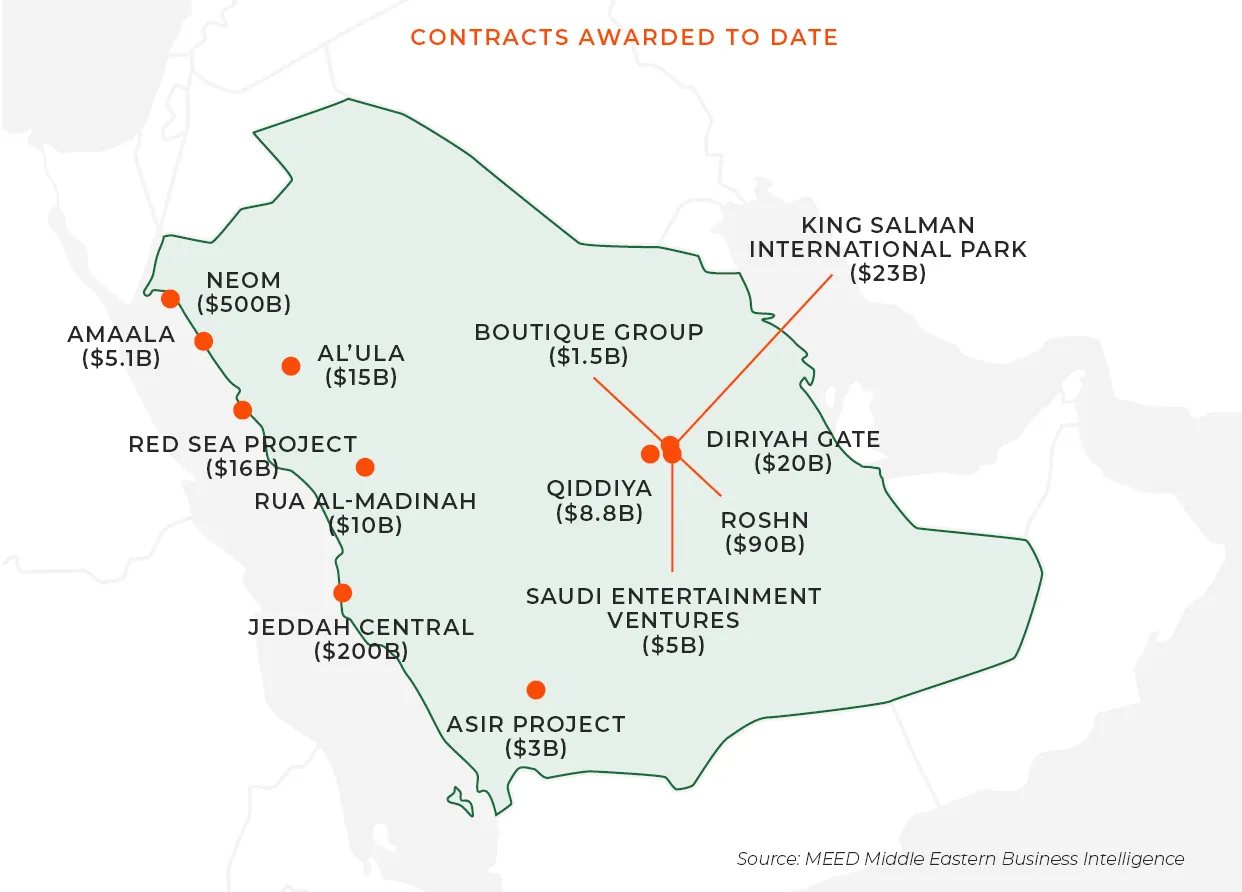

This rapid expansion is happening alongside more than 5,000 active construction projects worth around USD 819 billion. Mega-projects like NEOM and The Line are pushing traditional players to modernize fast. For many, the question is no longer whether to digitalize, but how.

Buy vs Build: The Executive Logic Behind PropTech Acquisitions KSA

Building digital platforms internally is slow and risky. Buying proven technology is faster and safer. This logic explains the global “Tech-for-Traditional” acquisition wave.

In one key year, construction technology startups raised around USD 357 million in venture funding. In the same period, incumbents spent about USD 2.2 billion acquiring them. That is a six-to-one gap.

The message is clear. Traditional firms allow startups and investors to fund experimentation. Once solutions work, they step in with large acquisition checks. These are not small pilot deals. Only eight M&A transactions accounted for the full USD 2.2 billion, showing that buyers prefer transformative acquisitions over incremental partnerships.

Why Data-Heavy Platforms Attract Buyers

Global analysis of more than 7,000 PropTech firms shows a clear pattern. Acquisitions cluster around platforms built on data, analytics, and workflows. These are not simple apps. They are digital operating systems for real assets.

In PropTech, solutions focused on “Living” and “Managing” functions represent around 79 percent of all acquisitions tracked globally. This shows where value lies. Established developers and operators want tools that run daily operations, not experimental features.

This same pattern is shaping PropTech acquisitions KSA, where scale and complexity demand reliable systems that can be plugged into existing operations.

Read Also: M&A Outlook Q3: Reform Momentum Builds in Saudi

Why Saudi Arabia Is a Hotspot

Venture investment in Saudi PropTech reached around USD 9 million in 2023, rising about 35 percent year on year. The Kingdom recorded more PropTech deals than any other market across the Middle East, Africa, Pakistan, Türkiye, and Southeast Asia in that period.

At the same time, Saudi Arabia is planning over 660,000 new housing units and more than 13 giga-projects. This creates long-term demand for software that standardizes processes, manages assets, and optimizes logistics.

For incumbents, acquiring technology is the fastest way to meet these needs at scale.

Read Also: MENA Merger Trends: Saudi Clears Deals in 4.1 Days

2026 Targets: Profitable B2B SaaS

The most attractive M&A targets heading into 2026 are profitable B2B SaaS companies serving construction and real estate. These platforms already generate revenue. They manage critical data. And they integrate deeply into workflows.

This combination offers immediate productivity gains and lower risk. It also explains why acquisition spending often exceeds venture funding in this sector. Value is captured at the point of acquisition, not experimentation.

Strategic Guidance for Navigating PropTech Acquisitions KSA

As PropTech acquisitions KSA accelerate, understanding where value truly sits becomes essential. Saudi Arabia M&A by Eurogroup Consulting, with 40 years of distinguished experience, excels in delivering strategic consulting services with a strong focus on market research in Saudi Arabia. Its committed team provides deep insights and hands-on support, positioning Eurogroup Consulting as an essential partner for succeeding in the Kingdom’s rapidly evolving market landscape.

Talk to us for your needs in:

-

Due Diligence and Valuation Services

-

M&A Strategy and Advisory

-

Post-Merger Integration Management

-

Regulatory and Compliance Advisory

-

Market Entry and Expansion Consulting

-

Investment and Financial Analysis

-

In-Depth Market Survey for M&A

-

Market Intelligence and Insights in M&A

-

Feasibility Study and Assessment in M&A

-

Saudi M&A Benchmarking