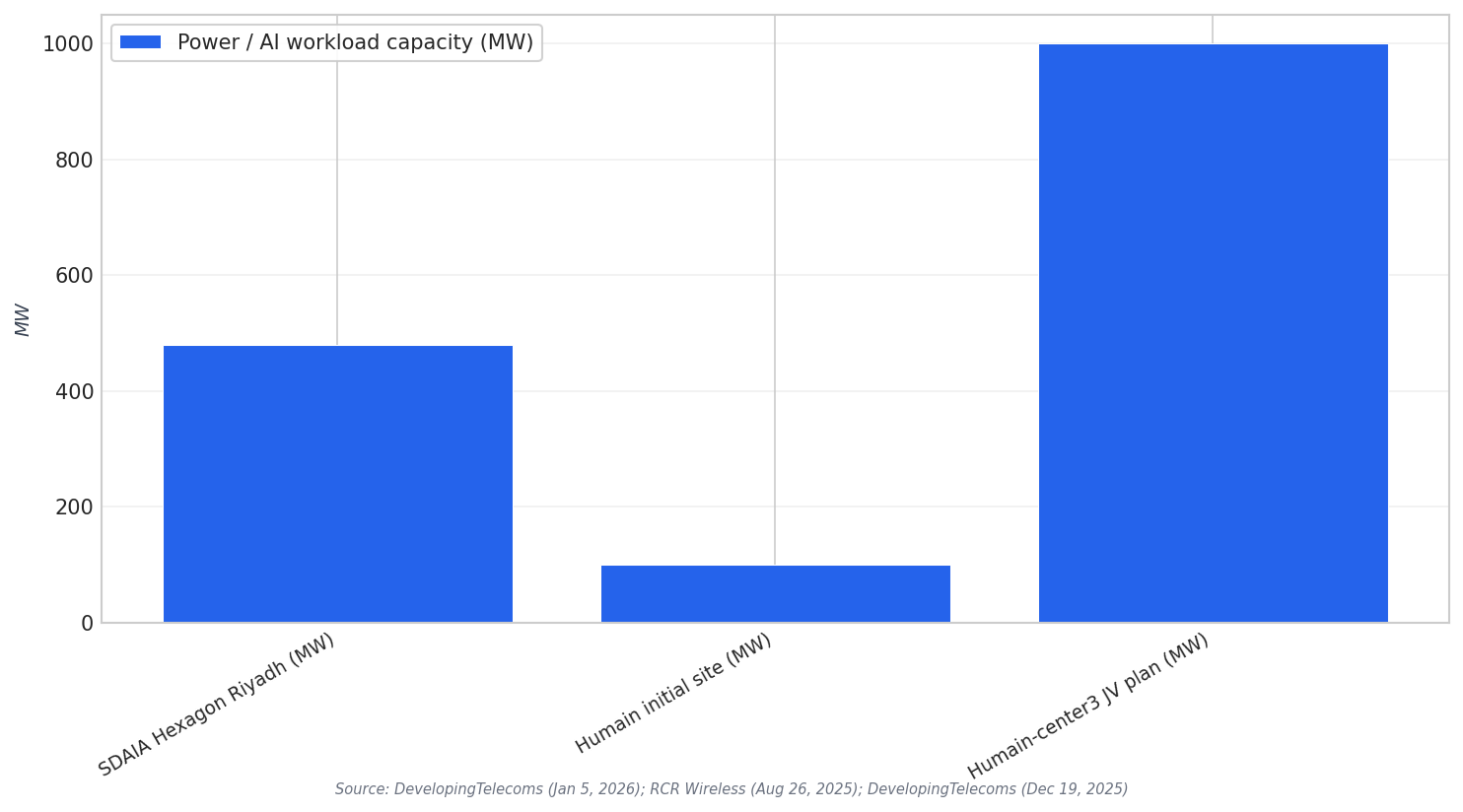

Hexagon’s Riyadh move is being read as more than a construction milestone. Work has begun on the Saudi Data and Artificial Intelligence Authority’s (SDAIA) Hexagon data centre in Riyadh. Developing Telecoms described it as the world’s largest government data centre. The certified Tier IV design will ultimately occupy 2.78 million square metres and have a power capacity of 480MW. Against the backdrop of big platform-style partnerships in the Kingdom, the project helps define a new Saudi AI data center M&A playbook, built around scale, anchor customers, and repeatable partner structures.

One pillar of that playbook is the rise of Humain. CNN reported that Humain is owned by the Kingdom’s nearly $1 trillion sovereign wealth fund. The same report said Humain plans to build up to six gigawatts in data center capability across the country by 2034 and has partners including Nvidia, AMD, Amazon Web Services, Qualcomm and Cisco. RCR Wireless, citing Bloomberg, added that Humain started building its first data centers in Riyadh and Dammam, with operations expected to begin in early 2026, and that each facility is set to launch in the second quarter of 2026 with an initial capacity of up to 100 megawatts.

Capital stacking is another pillar. CNN reported that Humain announced a $3 billion deal with Blackstone to build data centers in the Kingdom. Separately, PitchBook reported that Humain was in early discussions with private equity firms, including Blackstone and BlackRock, about committing “significant capital” to data centers and related infrastructure, citing anonymous sources via Bloomberg. Taken together, this creates a template for how large Saudi AI infrastructure projects can attract private capital alongside state-backed priorities, while still keeping platform control aligned with national entities and anchor programs.

A Repeatable JV-and-Partner Model Is Taking Shape

Saudi AI data center M&A is not only about acquisitions. It is also about joint ventures that behave like M&A in practice by bundling assets, customers, and execution capacity. Developing Telecoms reported that stc group formed a strategic joint venture with Humain through stc’s digital infrastructure subsidiary center3. The JV plans to develop and operate next-gen infrastructure capable of hosting up to 1GW of AI workloads. Total Telecom reported that center3 unveiled plans to expand to a total capacity of 1 Gigawatt by 2030, after investing approximately $3 billion already and planning an additional $10 billion into new hyperscaler-ready data centres.

Partnerships then extend the stack into equipment, cooling, and specialized buildouts. RCR Wireless noted talks centered on thermal management cooperation for what is expected to become the Middle East’s largest net-zero AI data center under construction by Saudi firm DataVolt, building on an MoU positioning LG as a strategic partner. Meanwhile, Developing Telecoms said Humain announced a flurry of deals with companies like Adobe, Amazon Web Services, xAI and Luma AI, and reported that Humain and AirTrunk established a partnership to build data centres in Saudi Arabia. The Hollywood Reporter added that Luma will have access to large Saudi-based data centers aiming to generate 2 gigawatts of computing power.

This playbook is forming in a competitive regional arena. CNN reported that the UAE has G42 and secured a landmark deal with the Trump administration to build “Stargate UAE,” described as a sprawling $500 billion data center project billed as the largest outside the United States, with help from OpenAI, Oracle, Nvidia and Cisco. Inside that context, Saudi projects such as SDAIA’s Hexagon facility in Riyadh, Humain’s buildout plans, and the center3 JV show a consistent strategy: combine sovereign backing, private capital, and industrial partners to accelerate delivery and lock in long-term compute capacity.

The numbers below illustrate how this ecosystem spans from individual facilities to multi-gigawatt national plans, and from government anchors to platform JVs. They use only capacity figures explicitly cited in the sources, and they highlight why deal structures are clustering around measurable compute and power commitments rather than vague innovation claims.

What does “Saudi AI data center M&A” mean in this context?

What are the key specs of the SDAIA Hexagon data centre in Riyadh?

How big is Humain’s data center ambition?

What is the Humain and center3 joint venture planning to host?

How does Saudi Arabia’s push compare with the UAE’s Stargate UAE project?

Talk to us for your needs in:

-

Due Diligence and Valuation Services

-

M&A Strategy and Advisory

-

Post-Merger Integration Management

-

Regulatory and Compliance Advisory

-

Market Entry and Expansion Consulting

-

Investment and Financial Analysis

-

In-Depth Market Survey for M&A

-

Market Intelligence and Insights in M&A

-

Feasibility Study and Assessment in M&A

-

Saudi M&A Benchmarking