Saudi quick commerce is moving into a new phase. Rabbit says it is building “Rabbit Saudi Arabia by Saudi hands,” and it officially launched operations in the Kingdom in early 2024, starting with Riyadh. Early users in Riyadh show weekly reorder rates comparable to Rabbit’s more mature Egyptian market, which signals strong early product-market fit. This kind of traction raises the pressure on other players to defend their turf, and it often turns normal competition into deal-driven “hyperlocal wars.”

The market signals are strong. Government sources put Saudi e-commerce revenues at approximately SAR 211 billion in 2024. Payments are also shifting fast. Electronic payments reached 79% of all retail transactions in 2024, and the government target of 70% cashless transactions has already been exceeded. On the supply side, hyperlocal delivery growth is linked to instant and same-day delivery demand, plus expansion of dark stores and micro-fulfilment centres.

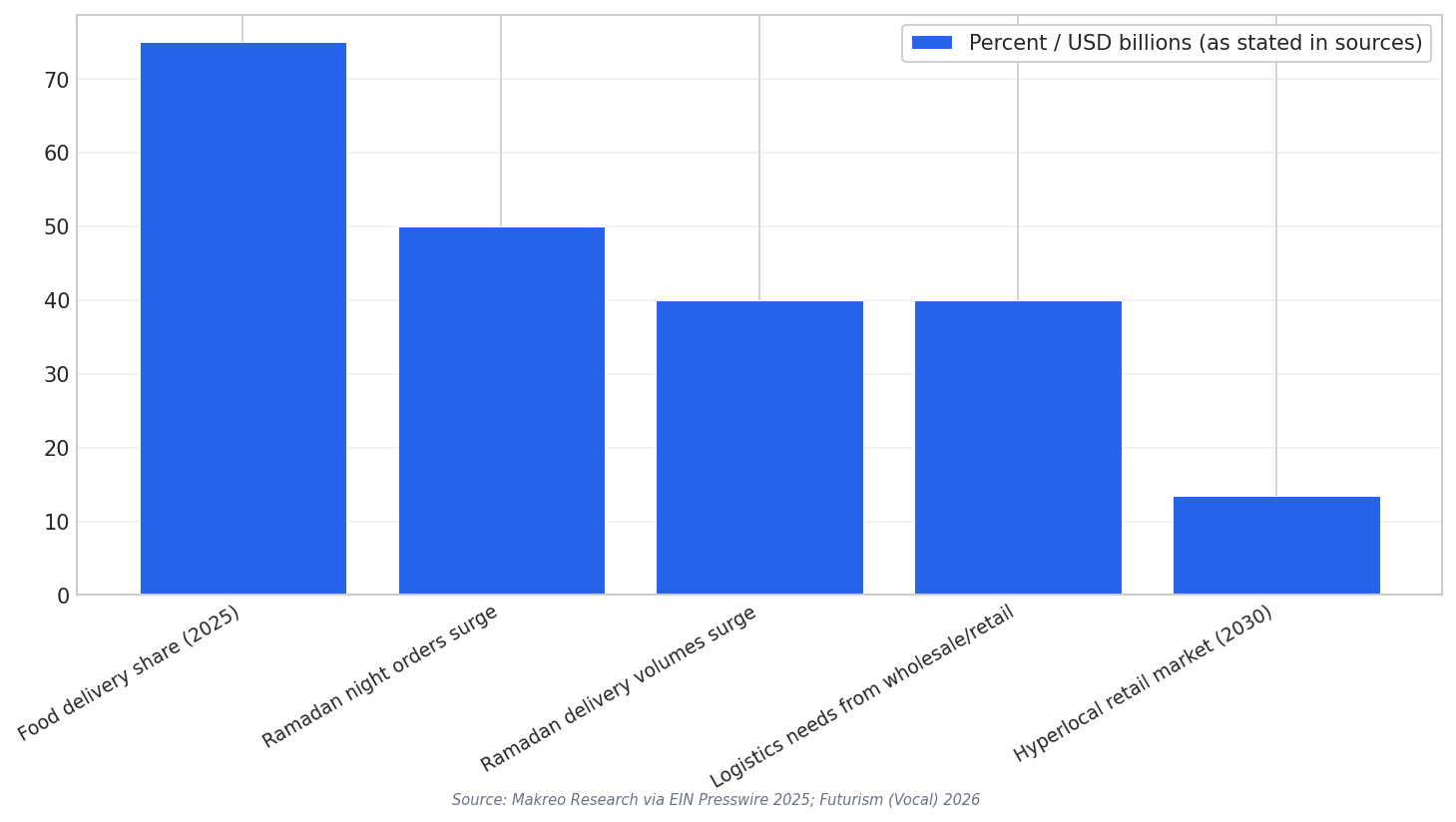

Here are five concrete data points that show how demand, infrastructure, and logistics are stacking up: food delivery contributed over 75% of Saudi hyperlocal market revenues in 2025; Ramadan night-time order volumes surged by nearly 50%; delivery volumes surged 40% during Ramadan for apps like HungerStation, Jahez, and Nana; roughly 40% of Saudi logistics requirements stem from wholesale and retail trade sectors; and the hyperlocal retail market alone is projected to reach USD 13.5 billion by 2030.

Why Rabbit’s Playbook Can Trigger M&A Instead of a Price War

Rabbit’s model depends on operational speed and tight inventory placement. Dark stores, also called micro-fulfillment centers or dark warehouses, exist only to handle online orders. When one player starts hitting strong reorder rates and keeps “ultra-fast service” standards, rivals often respond by scaling faster. But in hyperlocal delivery, scaling is not only marketing. It is warehouses, replenishment cycles, and middle-mile transport. Buying or investing can be faster than building everything from scratch.

The deal signals are already visible in the sector. In 2025, Jahez made a strategic, undisclosed investment in Doos, a Saudi quick-commerce platform established in 2023, to expand cloud stores across Riyadh and Jeddah. In parcel logistics, DHL eCommerce formed a joint venture with AJEX Logistics Services to acquire a minority share in a Saudi Arabia-based parcel logistics company. These moves fit a market where competition is intensifying beyond food and into essentials, fresh produce, and lifestyle categories.

This is where Saudi e-commerce acquisitions 2026 becomes a realistic expectation, even without public deal values. Rabbit entered the Saudi market with plans to deliver 20 million products across all major cities by 2026 and set up its regional headquarters in Riyadh. If several platforms chase the same promise of instant delivery, M&A and strategic investments become a way to lock in capacity, locations, and loyal customers, especially when loyalty programs and dark-store expansion are core growth drivers.

What is pushing Saudi e-commerce acquisitions 2026 in hyperlocal delivery?

What makes Rabbit different in Saudi Arabia?

Why do dark stores matter in quick commerce?

How big is e-commerce in Saudi Arabia based on the sources?